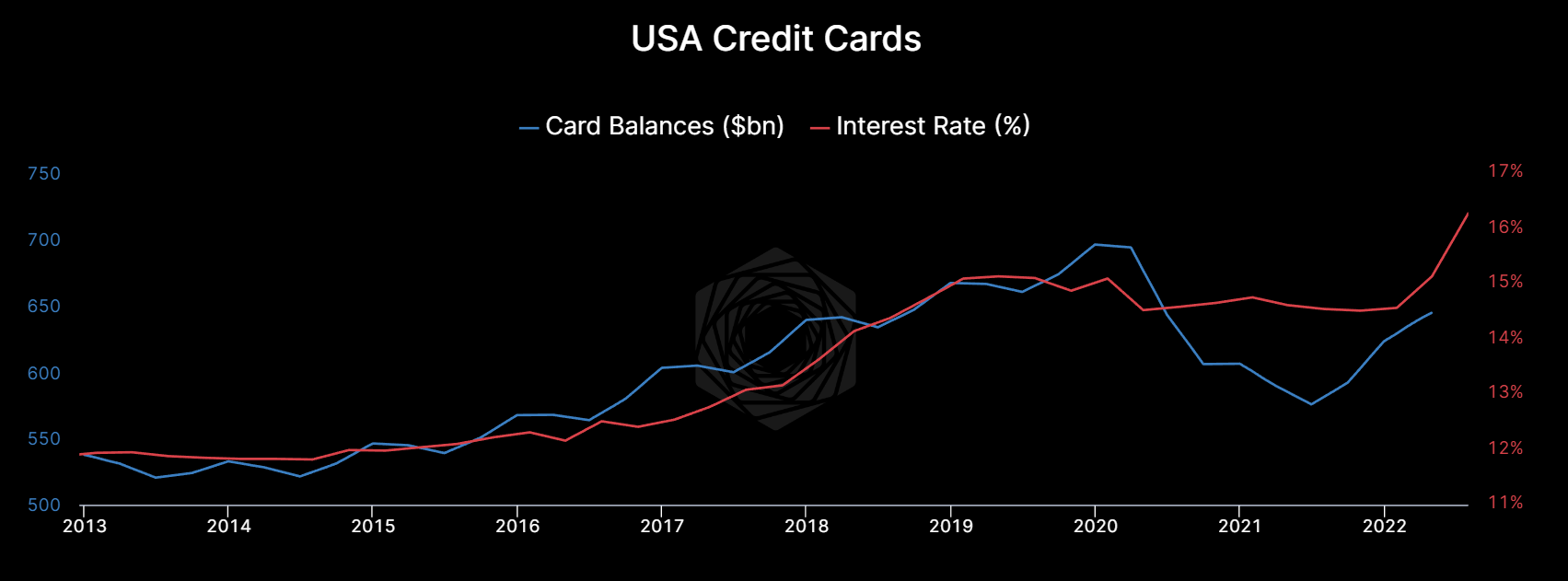

USA Credit Cards: Card Balances v. Interest Rate [OC]

USA Credit Cards: Card Balances v. Interest Rate [OC]Submitted by rosetechnology t3_10axob4 in dataisbeautiful

Square_Tea4916 t1_j49bw7f wrote

Reply to comment by joongoon543 in USA Credit Cards: Card Balances v. Interest Rate [OC] by rosetechnology

Assuming you mean a 1% Charge-off rate. Interchange is peanuts compared to what most banks make in fees/interest. I’ve worked at one of the largest Super Regional bank and a global bank spinning up card programs in Europe and North America and can tell you without a doubt the most profitable program is raising credit limits to increase outstanding balances.

joongoon543 t1_j49jnzy wrote

No, consumer loans that aren’t classified as real estate are less than 5% of our total loan portfolio. It’s extremely rare we have to charge off a consumer loan.

Come on man, if you actually worked at a bank of that size then there’s no way you would say interchange is “peanuts.” Chase made 20 billion from interchange and 51 billion in credit card interest in 2019. Calling that peanuts is insane.

Square_Tea4916 t1_j49q1ik wrote

They have to spend all that interchange in rewards and partnerships to maintain their customer base. Not to mention all the operational costs in servicing, disputes, and fraud. You can’t run a credit card business successfully on just interchange and be profitable. I don’t know a single bank where interchange outweighs interest even if their entire customer base is super prime.

The truth is… credit cards have become a bet on missed payments and overspending. For every 1 customer who genuinely needed “short-term liquidity” to cover for basic needs there’s 20 to 30 customers blowing stacks on the latest influencer’s merchandise or booking an expensive trip to live like royalty.

Viewing a single comment thread. View all comments