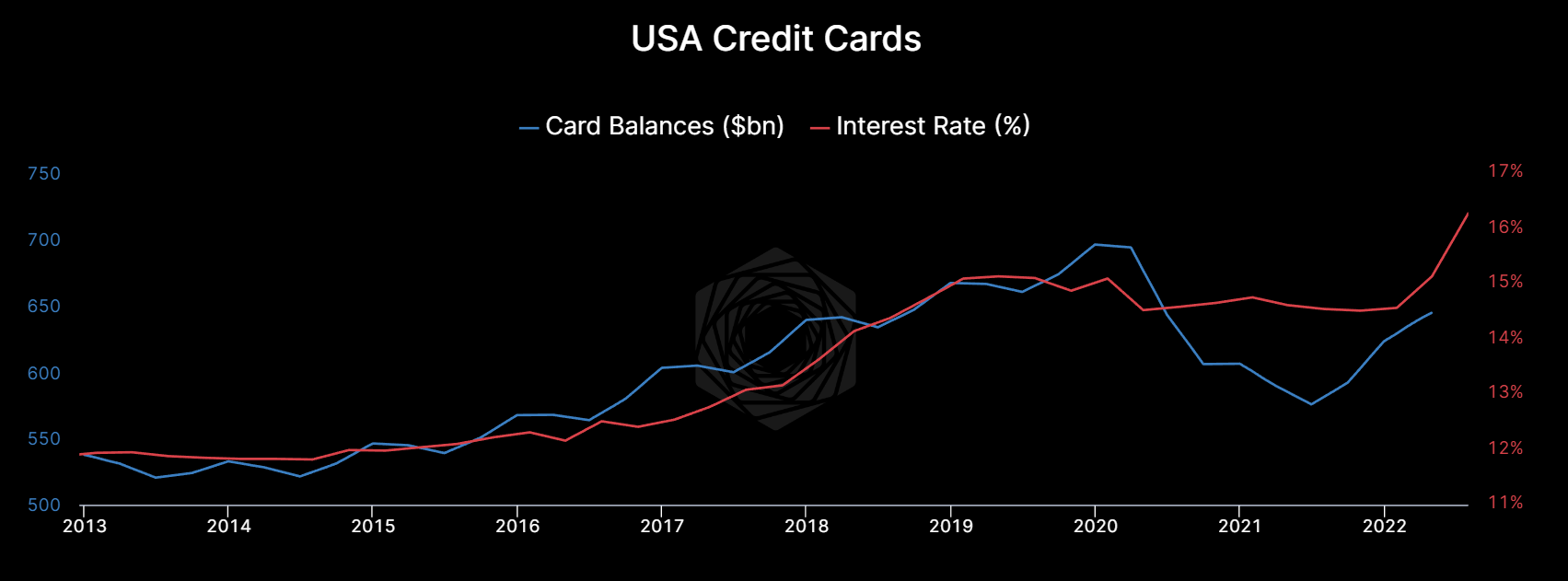

USA Credit Cards: Card Balances v. Interest Rate [OC]

USA Credit Cards: Card Balances v. Interest Rate [OC]Submitted by rosetechnology t3_10axob4 in dataisbeautiful

joongoon543 t1_j491f0u wrote

Reply to comment by Square_Tea4916 in USA Credit Cards: Card Balances v. Interest Rate [OC] by rosetechnology

Credit analyst for a bank.

You’re wrong. We don’t like increasing interest rates and it usually doesn’t have a large effect on net earnings. Although we collect more interest our default rate climbs and it usually wipes out any gains we make. In fact, a rising rate environment can lead to increased bank consolidation because banks with poor management and underwriting standards have their default rates climb faster than interest payments can cover. This leads to a bigger bank buying them out or worst of all the FDIC shutting them down and auctioning them off to another bank.

Furthermore, what you call “financially illiterate” are often people dealt a bad hand or in a really hard place (minorities especially). What do you want us to do? Return to a system that basically red lines entire groups of people because they’re struggling? Lines of credit are extremely important for not only businesses but giving people some flexibility. There are absolutely people that can’t handle their debt and that’s exactly why banks have credit departments monitoring underwriting and making sure the bank is in compliance with the FDIC or other regulatory agencies.

Square_Tea4916 t1_j4952ch wrote

Lot of kool-aid there. How does your Bank’s Credit Card make money? Just curious.

joongoon543 t1_j4981nw wrote

The bank offers several different lines of credit. The most common ones are HELOCs, and business LOCs. We offer credit cards but obviously we use Mastercard or Visa for our consumer credit card providers. We make money from credit card transactions. When you swipe a card the business gets charged for a swipe and we get a certain % of that. We obviously make money from interest.

Most medium sized regional banks like mine (total loan portfolio of $1 billion - $5 billion) make 75% of their income from businesses. Consumer loans just aren’t a money maker for us. Credit card debt is less than 1% of our portfolio, auto loans are around 2%.

Square_Tea4916 t1_j49bw7f wrote

Assuming you mean a 1% Charge-off rate. Interchange is peanuts compared to what most banks make in fees/interest. I’ve worked at one of the largest Super Regional bank and a global bank spinning up card programs in Europe and North America and can tell you without a doubt the most profitable program is raising credit limits to increase outstanding balances.

joongoon543 t1_j49jnzy wrote

No, consumer loans that aren’t classified as real estate are less than 5% of our total loan portfolio. It’s extremely rare we have to charge off a consumer loan.

Come on man, if you actually worked at a bank of that size then there’s no way you would say interchange is “peanuts.” Chase made 20 billion from interchange and 51 billion in credit card interest in 2019. Calling that peanuts is insane.

Square_Tea4916 t1_j49q1ik wrote

They have to spend all that interchange in rewards and partnerships to maintain their customer base. Not to mention all the operational costs in servicing, disputes, and fraud. You can’t run a credit card business successfully on just interchange and be profitable. I don’t know a single bank where interchange outweighs interest even if their entire customer base is super prime.

The truth is… credit cards have become a bet on missed payments and overspending. For every 1 customer who genuinely needed “short-term liquidity” to cover for basic needs there’s 20 to 30 customers blowing stacks on the latest influencer’s merchandise or booking an expensive trip to live like royalty.

Viewing a single comment thread. View all comments