[OC] - US Yield Curve, mean yield curve spread, and percent of all yield curve combinations that are inverted

[OC] - US Yield Curve, mean yield curve spread, and percent of all yield curve combinations that are invertedMetricT OP t1_ixuuzab wrote

Tools: RStudio

Data: FRED (current/historical bond yields and Fed rate), MarketWatch (up-to-the-minute bond yields), Robert Shiller (historical 10 year bond yields)

R Source: https://github.com/MetricT/R_Code/blob/main/EconFinance/Yield_Curve_Minidash.R

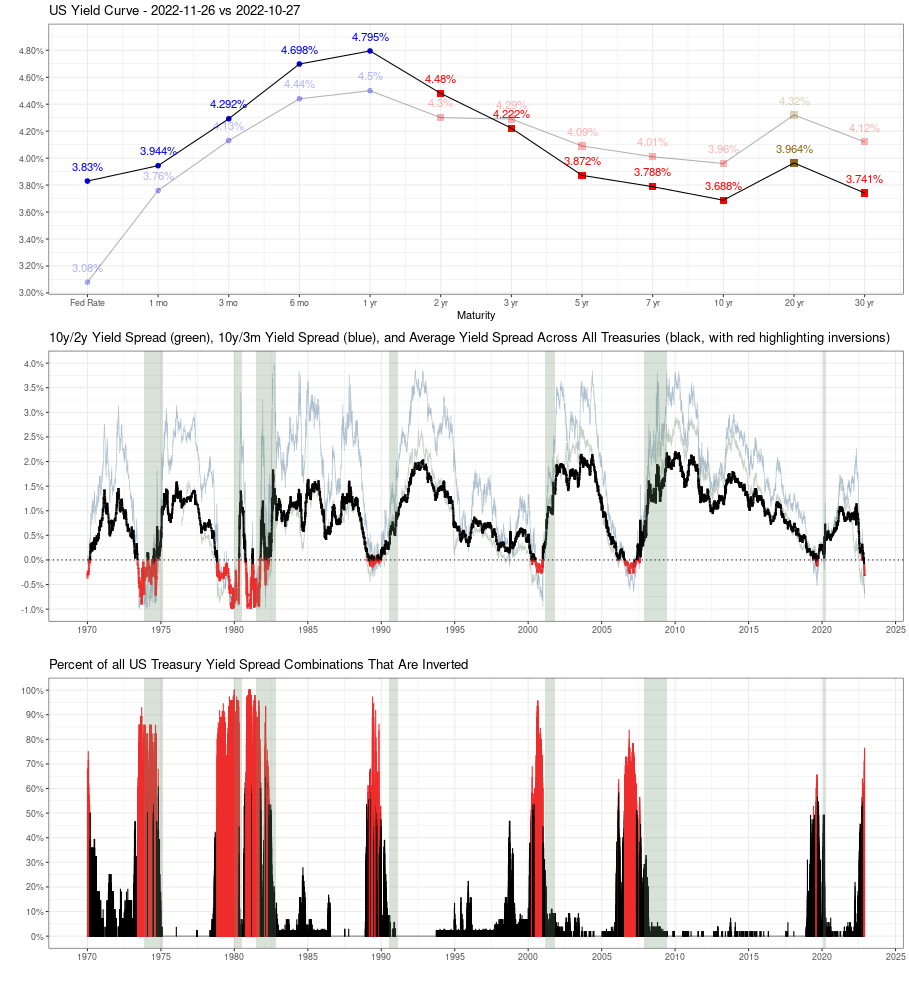

I have previously posted a graph that shows both the number of inverted yield curves as well as the mean yield spread across all durations. I have found that those measures avoid a false positive/negative or two that affect the traditional 10y/2y and 10y/3mo yield curve spreads. Which makes sense. The latter are only looking at one particular yield spread, while the former are looking at inversions along the entire yield curve, and do a better job of capturing the overall distortion of the yield curve at a given time.

You can see in the top graph that the yield curve is "see-sawing". Long-term yields are falling as Smart Money rushes to lock in their investments over the long term before a recession gets here. Short-term yields are rising since fewer people are buying them. The yield curve is "humped" but not yet inverted, but at the rate it's shifting, there's a good chance it will invert early in 2023.

The middle graph shows the average yield spread across all Treasury maturities, compared to the more common 10y/2y and 10y/3mo spreads. I've left it off this dashboard, but when the average yield curve goes "red", the Fed has historically instantly stopped raising rates, except during the high-inflation 70's. So it'll be interesting to see what they do this time.

The bottom shows the percent of all yield spread combinations that are inverted. Today there are 11 Treasury maturities (1mo, 3mo, 6mo, 1yr, 2yr, 3yr, 5yr, 7yr, 10yr, 20yr, 30yr), though the exact number has changed over time. A little math shows that 11 maturities yields 55 different yield spread combinations, though again the exact number has changed over time. Graphing the percent that are inverted helps offer a apples-to-apples comparison across time, and highlights times (like now) when the yield curve is highly distorted.

I promised that I would try to find time to post the script source by the end of the year, so Merry Christmas! It runs fine on my Linux RStudio Server and Windows RStudio, so hopefully it will run on your computer too.

jbrandon t1_ixuzykj wrote

Ok. Thank you. What does this mean for the average working class?

MetricT OP t1_ixv0g9o wrote

The "will we/won't we have a recession" indicator is pointing solidly towards "we will". That said, signs are a recession will be relatively mild since it's "artificially" created by the Fed rather than a normal business cycle recession. I'm more concerned about the recovery than the recession, as I suspect it is likely to be slow and painful.

ShankThatSnitch t1_ixvasp7 wrote

The reason the yield curve is important, is it tells you how the liquidity will be in the financial system. If you don't know, liquidity basically means the availability of money, and the ease of which it moves around the financial system/economy.

If you look at the first graph on the left, you see the "Fed Rate". This is the rate the federal reserve sets, that determines what banks charge each other to lend money to one another. everything to the right of that are the different treasuries that the US gov't sells, with different maturities, ranging from 1 month to 30 years. In a normal, healthy economy/financial environment, the shortest end of the curve is supposed to be very close to the fed funds rate, and should slope upward the further to the right it goes, because the longer you are loaning your money out, the more risk you are taking, and the more return you should get.

The short end of the curve (1month - 2 years) is heavily influenced by the fed funds rate, and where the market believes the fend funds rate will be going forward in those time frames. the medium/long end (3 year to - 30 year), is determined mostly by the markets expectation of where economic growth and inflation are headed longer term. So this chart basically says, the market thinks the fed will keep increasing rates over the next 9-12 months, but will have to ease, as the economy starts to significantly slow after that, and that our economy is going to remain at slow growth for the foreseeable future.

TL:DR. The reason this curve is such a good predictor of recession, is because bank borrow money from the fed and eachother at the Fed Rate, and loan out money at the longer rates, for car loans, mortgages and business loans. If it costs more for banks to borrow, thank they can charge for long term loan products, they stop lending, which mean businesses invest less, which means less hiring. Regular people are not able to borrow as easily for cars, homes...etc. The banks instead go out and start buying long term treasuries instead to get a guaranteed return from the gov't, which accelerates the inverted yield curve and economic slowdown. So we are basically near 100% chance of recession, and it will remain that way until the fed reverse and brings the front end of the yield curve back down.

jbrandon t1_ixvd8ka wrote

Ok. Thank you. What tools does the government have to fix this yield curve problem?

ShankThatSnitch t1_ixvf65s wrote

Well, the only real tool is the fed lowering the Fed rate. The fed could also start doing yield curve control, by buying up specific US treasuries, but this is not a real solution, and just kicks the can down the road. This is essentially what the Bank of Japan has been doing, and is arguably a large factor in why they have super slow economic growth for the past 10-20 years. The other major factor, is their population is getting very old.

The issue with lowering the Fed rate right now, is that they could reverse progress on trying to get inflation under control. The fed and Gov't WANT to cause a recession, because it is a sure fire way to kill inflation. And the reason they would do that, is because the longer and worse inflation carry on, the more devastating the resulting recession will be. So they want to get it out of the way, cause a bunch of bankruptcies and defaults in the short term to kill inflation now, rather than have utter catastrophe later on.

A recession also fixes the yield curve, because is washes out a ton of bad debt, which is a drag on economic growth. Once a bunch of bad debt is cleared away, a new growth/debt cycle can start, and the curve will naturally return to a normalized curve.

​

You should watch this video by Ray Dalio, which breaks down the debt cycles in a very simple way, they makes it much easier to understand the big picture of all this stuff.

jbrandon t1_ixvfr51 wrote

Thank you. So the Fed rate is really the only tool the government has? I’m not a civics expert but aren’t there any other options that the executive branch can wield without needing to pass legislation?

ShankThatSnitch t1_ixvid3h wrote

Well, the Fed is not exactly part of the Gov't. In theory it is separate, but in practice it is more connected. The president can do certain things through executive order, to try and spur economic growth, but there is no guarantee it will work, or for how long. The simple fact is that the way the global financial/monetary system works, basically guarantees cycles of growth, followed by recessions.

There are a few cycles. The 10 year cycle, which is the basic growth cycle, then there is a generational cycle, which is based on major population generations, and when they become earners or start retiring etc. because if causes certain spending habits to change on a large scale, like everyone in a specific generation starting to buy houses and have kids, which comes with a ton of economic activity. Then there is the long term debt cycle, which is more like 70-100 years, and involves bigger economic trends that also include sovereign debt, and the stability of nations as a whole.

There are things that can be done to delay the cycles to an extent, but you can't prevent them from happening, because it all ties into how money and debt works. Watch the video, and you will understand a lot more.

Viewing a single comment thread. View all comments